Listen to the audio version of this article (generated by AI).

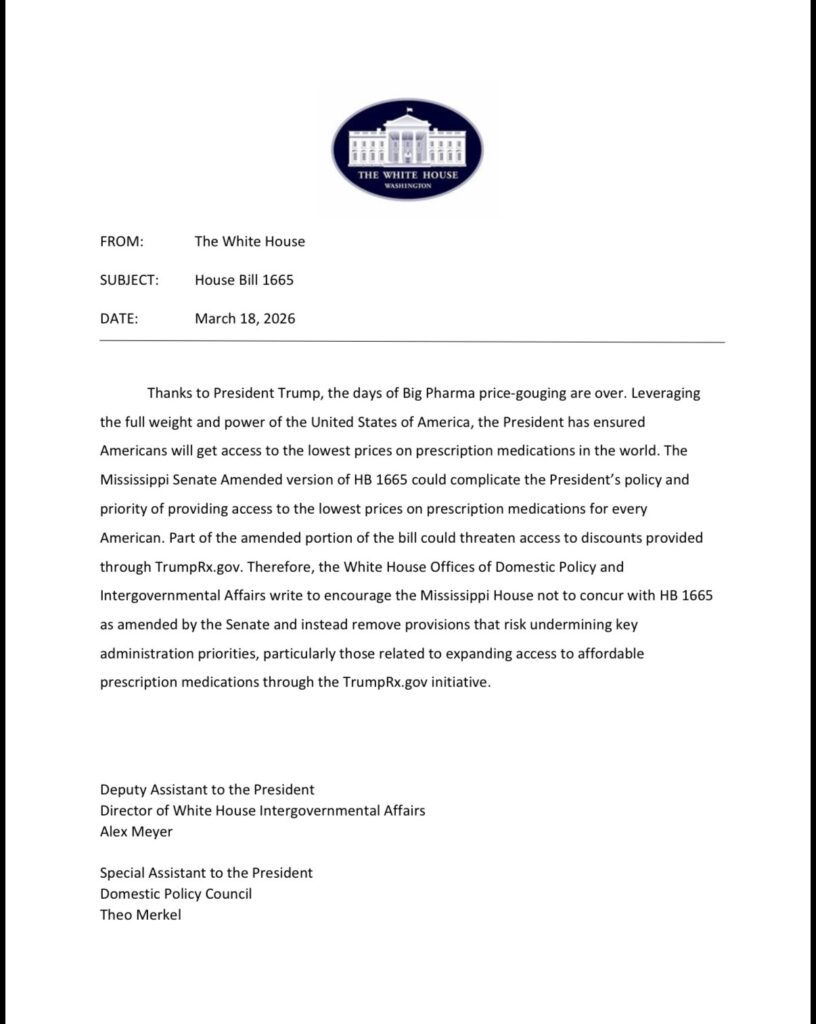

- HB 1665, as amended by the Mississippi Senate, would create an $11.29 dispensing fee for prescription drugs, likely adding hundreds of millions in new expenses for businesses and consumers. On Tuesday, the White House said “stop it.”

The Mississippi House of Representatives passed legislation earlier this year that provides for additional regulation of the pharmacy benefits managers (PBMs) that negotiate the amount your insurance will pay for prescription drugs.

Last week, the Mississippi Senate dramatically amended HB 1665 to add an $11.29 “dispensing fee” to every prescription filled in the state. The cumulative effect of this new charge would be hundreds of millions of dollars annually in new expense, higher drug costs, higher insurance premiums, and higher out of pocket costs for every working Mississippian.

Why would your elected representative consciously vote to artificially raise your already sky high health insurance premiums?

You’ll have to ask them, but late Tuesday, the Trump White House called on legislators to stop the nonsense. A memo sent by two of the President’s domestic policy advisors, warned that the Senate’s amended version of HB 1665 “could complicate the President’s policy and priority of providing access to the lowest prices on prescription medications for every American.” It urges House members not to concur with the Senate’s changes.

Understanding the Issue

Health insurance is expensive. That’s true for private sector workers. It’s true for state workers. Many employers cover at least some of that expense, though the end consequence of rising benefits cost is smaller salaries.

There are a great multitude of reasons for the exorbitant cost of health insurance, including perverse regulatory incentives and market interference.

The industry, itself, actually has relatively low reported profit margins. The primary driver of the cost of health insurance is the underlying cost of care.

One of the largest expenses covered by any health insurer, whether through individual plans, under an employer-sponsored ERISA plan, or through government programs like Medicare and Medicaid is prescription drugs.

How prescriptions are paid for is complex. Years ago, insurance companies created entities called “pharmacy benefits managers” designed to negotiate with both drug manufacturers and pharmacies to keep the price of drugs in check.

PBMs get paid by negotiating rebates with drug manufacturers for prescriptions added to “formularies” or lists of approved drugs. Think of it as a volume practice, where PBMs offer shelf space in exchange for lower wholesale prices.

PBMs also get paid through a somewhat controversial practice called “spread pricing.” Under spread pricing, the insurance company agrees to pay a certain amount for a drug and the PBM takes a residual “cut” before paying the rest to the pharmacy. All of this is negotiated on both ends of the deal.

Independent pharmacists question these practices, arguing they create downward pressure on their margins and makes it hard to stay in business. They also question “vertical integration” practices where a single parent company owns the insurance company, the PBM and the large chain pharmacies that PBMs sometimes steer patients to for prescriptions.

CVS Health Corporation owns Aetna (insurance), CVS Caremark (PBM) and CVS pharmacies, for example. As an aside, kudos to whoever lobbies for CVS in Mississippi. The changes made by the Senate, discussed below, could represent an “unwitting” massive competitive advantage for it.

Negotiations, Third Parties and Middlemen

The amount paid to the pharmacy per drug is based on a negotiation between the PBM and the pharmacy. For larger pharmacies, like Kroger, this is a direct negotiation. Smaller, independent pharmacies hire “pharmacy services administration organizations” or PSAOs to negotiate on their behalf. These PSAOs are owned by the nation’s largest drug wholesalers.

In a nutshell, the negotiation of the prices paid to your neighborhood pharmacy when they sell a drug comes down to a PBM, owned by an insurance company, and a PSAO, owned by a drug wholesaler.

When this same fight broke out last year, I said it was a national cartel war, Mississippi was being used as a proxy, and legislators should proceed with caution before mucking up something they don’t understand.

Independent pharmacists got big mad at me. Their misapprehension was the idea that I was calling them a cartel. No. They are pawns in a big boy war and understandably frustrated by it. Though it was funny to get attacked with identical talking points, and invited to debate on national podcasts, by people all over the country (and outside of it) who were very insistent that this is not a national cartel fight.

The Wall Street Journal did some excellent reporting on the nature of the cartel war over prescription drugs and drug pricing in December. Drug manufacturers spent over $31 million lobbying and on advocacy last year, training much of their ire and resources on PBMs through the funding of “local” astroturf opposition. “Pharmaceutical companies have been pretty successful in shifting a disproportionate amount of blame to the PBMs,” said Steve Knievel, a health-policy expert with Public Citizen, a nonprofit consumer-advocacy group.

Legislature’s Job in Changing Business Landscape is to First Do No Harm

Independent pharmacists’ solution to the quagmire they find themselves in is to ask the state legislature to effectively invalidate contracts negotiated between Mississippi’s employers, including the state itself, and their insurance providers — robbing businesses of the benefit of the bargain they struck and driving up cost on nearly all Mississippi workers.

America’s business climate is dynamic. For the last several decades, we have been in a climate of consolidation. This consolidation allows bigger players, because of volume, to operate with economies of scale. Consumers often get better prices than they otherwise would because of it, but “mom and pops” have a harder time competing. It’s the Wal-Mart effect. Independent pharmacists, who have lower volumes and less negotiating power, are trying to manage.

But it is not the job of the legislature to ensure that a specific segment of an industry, operating with a specific business model, survives. This is especially true when the price of doing so is higher healthcare costs on everyone in the state.

It should be noted that there are plenty of independent pharmacies in Mississippi kicking butt financially because they’ve figured out how to adjust their business model.

Common Core Math

Still, the lobby pushing the changes adopted by the Senate is asking legislators to adopt a new math — one where statutorily raising dispensing fees by 1000 percent or more somehow saves customers money.

They point to changes made by the Division of Medicaid that included adopting the same $11.29 dispensing fee and argue that Medicaid experienced savings after. It’s a comparison so dishonest it hurts. The root cause of Medicaid prescription savings was not the addition of a dispensing fees. That ate into the savings.

There are three primary “benchmarks” used in pricing the costs of prescription drugs. NADAC (National Average Drug Acquisition Cost) provides a survey-based estimate of actual pharmacy acquisition costs. WAC (Wholesale Acquisition Cost) is a manufacturer’s list price to wholesalers. AWP (Average Wholesale Price) is an inflated “sticker price.”

Prior to Medicaid’s change it was covering the cost of prescriptions using the extremely inflated average wholesale price (minus a negotiated discount). When it switched to using NADAC as its benchmark, the savings were dramatic. So much so that it could add the new dispensing fee and it still be less expensive than when it was using AWP. But the reason it became less expensive was not the addition of the dispensing fee. Again, that addition cut into what the savings would have otherwise been.

Commercial insurance does not negotiate coverage for prescriptions at the starting point of using the AWP benchmark, so any savings on the underlying cost of prescription drugs by switching to NADAC, as anticipated by the Senate’s amendment, will not be as dramatic as Medicaid’s. (Not every drug is priced by NADAC either). Such that when the dispensing fee is added, the Senate’s changes will not represent a savings, but at least nine figures in additional annual costs.

It’s apples and oranges.

Medicaid also has a vast array of built in advantages, ranging from being able to negotiate larger rebates, to limits on the number of prescriptions that are covered for any beneficiary (6), to the fact that the overwhelming bulk of the dispensing fee is covered by the federal government. Commercial insurers, and the people that pay their premiums, have none of those.

Elimination of Anti-Steering Provision

As alluded to earlier, one of the complaints independent pharmacists have against PBMs is that two of them are vertically integrated (a parent company that owns the insurer, the PBM and the PBMs preferred pharmacy).

The original house version of HB 1665 included “anti-steering” provisions that prohibited a PBM like CVS Caremark from pushing its customers to buy their prescriptions from a CVS pharmacy. As a matter of principle, this provision isn’t very free market (not that any of this is) and ignores the fact that vertical integration can result in lower prices for consumers. The Senate removed it.

However, removing it, in concert with the dispensing fee, could unwittingly (or wittingly) create a big competitive advantage for a vertically integrated pharmacy. Essentially the cost of the dispensing fee could be eaten on one or both sides of the ledger, allowing a vertically integrated pharmacy to offer lower overall drug costs.

Russ Latino