Consumption buoyed most of the growth in the first quarter as production slowed and job cuts increased.

A new report from the U.S. Commerce Department shows that growth thus far in 2023 has slowed. The key reason remains linked to Federal Reserve interest rate increases as it continues to attempt to tackle record high inflation.

To date, the Fed has raised the interest rate to the highest it has been in 16 years, increasing the rate by 4.75 percentage points since March 2022.

Some economic analysts are warning of the potential for stagflation, the result of high inflation and slow growth. Stagflation last gripped the U.S. economy in the late 1970s into the early 1980s – the last time inflation was as high as it has been in the nation.

The report released Thursday morning did not help to tone down those concerns about a return to stagflation, perhaps even a recession later this year, as it indicated that consumption buoyed most of the growth in the first quarter as production slowed and job cuts increased.

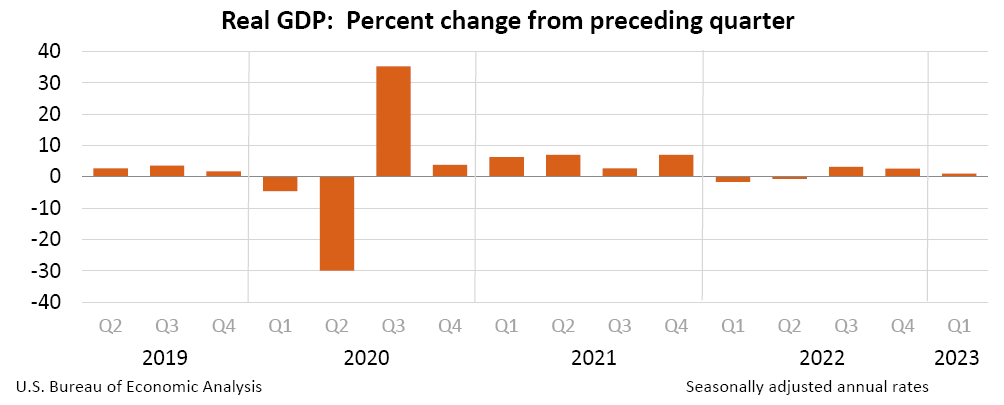

Real gross domestic product (GDP) increased at an annual rate of 1.1 percent in the first quarter of 2023, according to the “advance” estimate from the Bureau of Economic Analysis (BEA). In the fourth quarter of 2022, real GDP increased 2.6 percent.

BEA notes that the increase in the first quarter primarily reflected an increase in consumer spending that was partly offset by a decrease in inventory investment. The report stated:

The increase in consumer spending reflected increases in both goods and services. Within goods, the leading contributor was motor vehicles and parts. Within services, the increase was led by health care and food services and accommodations. Within exports, an increase in goods (led by consumer goods, except food and automotive) was partly offset by a decrease in services (led by transport). Within federal government spending, the increase was led by nondefense spending. The increase in state and local government spending primarily reflected an increase in compensation of state and local government employees. Within nonresidential fixed investment, increases in structures and intellectual property products were partly offset by a decrease in equipment.

The decrease in private inventory investment was led by wholesale trade (notably, machinery, equipment, and supplies) and manufacturing (led by other transportation equipment as well as petroleum and coal products). Within residential fixed investment, the leading contributor to the decrease was new single-family construction. Within imports, the increase reflected an increase in goods (mainly durable consumer goods and automotive vehicles, engines, and parts).

Compared to the fourth quarter, the deceleration in real GDP in the first quarter primarily reflected a downturn in private inventory investment and a slowdown in nonresidential fixed investment. These movements were partly offset by an acceleration in consumer spending, an upturn in exports, and a smaller decrease in residential fixed investment. Imports turned up.

BEA also reported that the price index for gross domestic purchases increased 3.8 percent in the first quarter, compared with an increase of 3.6 percent in the fourth quarter.

However, the White House did its best to portray calm, saying that the “American economy remains strong, as it transitions to steady and stable growth.”

“This past quarter, real personal disposable income increased and American consumers continued to spend, even as the overall pace of growth moderated,” President Joe Biden was quoted as saying in the Administration’s press release. “This follows reports that our economy added more than 300,000 jobs per month during the quarter, the unemployment rate remained near a 50-year low, and workforce participation for working-age Americans is the highest in 15 years.”

President Biden went to promote his “Investing in America agenda,” saying his Administration is seeking to rebuild the U.S. economy “from the middle out and the bottom up, following decades of failed trickle-down economic policies.”